One of the biggest reasons people buy Life Insurance is to provide financial protection for loved ones after death.

But many families wonder:

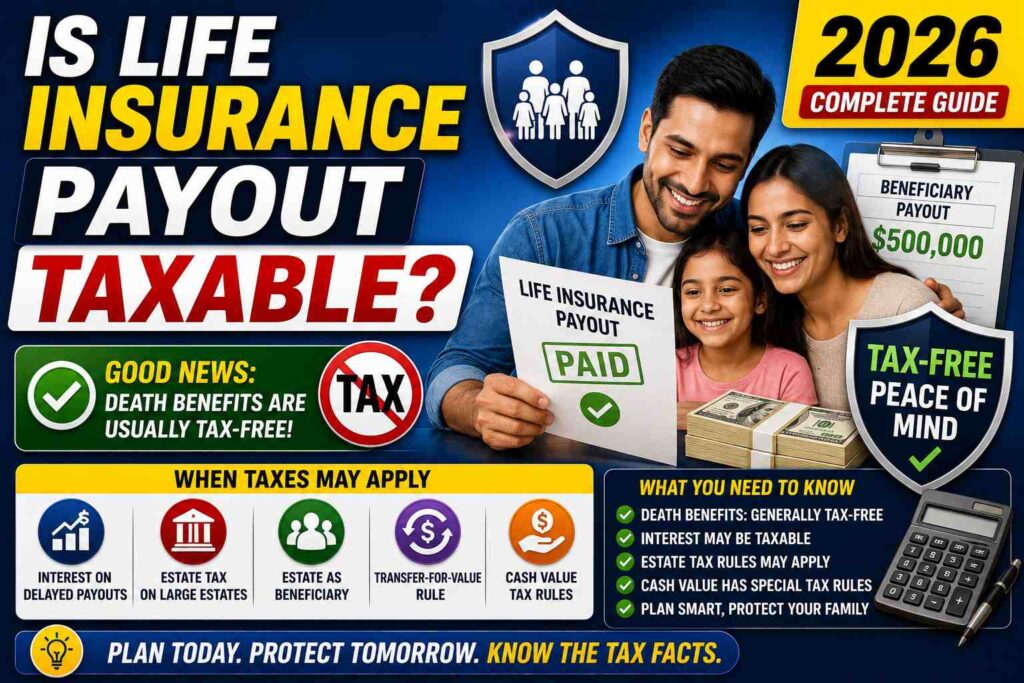

“Do beneficiaries have to pay taxes on life insurance payouts?”

The good news is:

In most cases, life insurance death benefits are not taxable.

However, there are important exceptions where taxes may apply.

In this complete 2026 guide, you’ll learn:

- When life insurance payouts are tax-free

- Situations where taxes may apply

- Estate tax rules

- Cash value taxation

- Interest taxation

- Inherited policy tax considerations

Are Life Insurance Death Benefits Taxable?

Usually, no.

When a beneficiary receives a life insurance death benefit as a lump sum, the payout is generally:

Federal income tax-free

This means beneficiaries usually do not pay income tax on the money received.

Simple Tax Formula

\text{Standard Life Insurance Death Benefit} \rightarrow \text{Usually Tax-Free}

Why Life Insurance Payouts Are Usually Tax-Free

Governments generally treat life insurance death benefits as:

- Financial protection

- Family support

- Compensation after death

rather than taxable earned income.

Example of a Tax-Free Life Insurance Payout

Suppose:

- A policyholder has a $500,000 life insurance policy

- They pass away

- The beneficiary receives the full payout

In most cases:

- The beneficiary receives the full $500,000 tax-free

Also Read: What Is a Deductible in Health Insurance? Complete 2026 Guide

Situations Where Life Insurance Payouts May Be Taxable

Although most payouts are tax-free, some situations can trigger taxes.

Interest Earned on Delayed Payouts

If the insurance company keeps the money temporarily and pays interest before distribution:

- The original death benefit is usually tax-free

- The earned interest may be taxable

Example

Suppose:

- Death benefit = $500,000

- Interest earned = $5,000

Tax treatment:

- $500,000 → usually tax-free

- $5,000 interest → potentially taxable income

Estate Taxes on Large Policies

Large estates may face estate taxes depending on:

- Estate value

- Local laws

- Ownership structure

If the policy owner’s estate exceeds estate tax thresholds, part of the payout could become taxable within the estate.

Estate Tax Formula

\text{Total Estate Value} + \text{Life Insurance Proceeds} = \text{Possible Estate Tax Exposure}

When the Estate Is Named as Beneficiary

Taxes may become more complicated if:

- The estate receives the payout instead of individual beneficiaries

This can:

- Increase estate size

- Potentially trigger estate taxes

- Delay distribution

Transfer-for-Value Rule

A life insurance payout may become partially taxable if:

- Someone purchases or transfers ownership of an existing policy for money or value

This is called the:

Transfer-for-Value Rule

Complex tax rules may apply in these situations.

Are Life Insurance Premiums Tax Deductible?

For personal life insurance:

Usually no.

Most individuals cannot deduct life insurance premiums on personal tax returns.

However, some business-related situations may differ.

Is Cash Value Life Insurance Taxable?

Whole Life Insurance and other permanent policies may build:

- Cash value

- Investment growth

The cash value itself usually grows:

Tax-deferred

This means taxes are generally postponed while the money remains inside the policy.

Can Borrowing Against Cash Value Be Taxable?

Policy loans are often:

Not taxable

as long as:

- The policy remains active

- Loan rules are followed

However, tax complications can occur if:

- The policy lapses

- The loan exceeds the policy basis

What Happens If You Surrender a Policy?

If you cancel or surrender a permanent life insurance policy:

- Gains above the premiums paid may become taxable

Example of Cash Value Taxation

Suppose:

- Total premiums paid = $50,000

- Cash surrender value = $70,000

Potential taxable gain:

70000 – 50000 = 20000

The $20,000 gain may be taxable.

Are Employer-Provided Life Insurance Benefits Taxable?

Sometimes.

Many employers provide group life insurance coverage.

In some countries:

- Coverage above certain limits may create taxable benefits for employees

Tax treatment depends on local tax laws.

Is Life Insurance Taxable for Beneficiaries?

Usually beneficiaries do not pay:

- Income tax

- Capital gains tax

on standard lump-sum death benefits.

However, taxes may apply to:

- Interest earned

- Estate-related situations

- Certain annuity structures

Life Insurance Payout Options and Taxes

Lump-Sum Payout

Usually tax-free.

Installment Payments

The principal may remain tax-free, but:

- Interest portions could become taxable

Annuity Option

Regular payments may include taxable investment growth portions.

Does State Tax Apply to Life Insurance?

Tax rules vary depending on:

- Country

- State

- Local laws

Some regions may have:

- Inheritance taxes

- Estate taxes

- Special insurance tax rules

How to Reduce Potential Taxes on Life Insurance

Name Individual Beneficiaries

Avoid unnecessary estate complications.

Use Trust Planning

Some wealthy families use:

Irrevocable Life Insurance Trust

to help reduce estate taxes.

Review Ownership Structure

Policy ownership affects tax treatment.

Consult Tax Professionals

Large estates or business-related policies may require expert advice.

Common Myths About Life Insurance Taxes

“All Life Insurance Is Tax-Free”

Not always. Interest and estate taxes may apply.

“Beneficiaries Always Pay Taxes”

Most beneficiaries receive tax-free death benefits.

“Cash Value Is Never Taxed”

Policy surrender gains can become taxable.

“Premiums Are Tax Deductible”

Personal life insurance premiums usually are not deductible.

Why Life Insurance Tax Rules Matter in 2026

As wealth, estate values, and financial planning strategies evolve, understanding insurance taxation becomes increasingly important.

Many families today use life insurance for:

- Income replacement

- Estate planning

- Wealth transfer

- Business protection

Understanding tax implications helps avoid costly mistakes.

Frequently Asked Questions (FAQs)

Is life insurance payout taxable income?

Usually no. Standard death benefits are generally tax-free.

Do beneficiaries pay taxes on life insurance?

Typically not on lump-sum death benefits.

Is interest earned on life insurance taxable?

Yes, interest portions may be taxable.

Can life insurance create estate taxes?

Yes, large estates may face estate tax exposure.

Are life insurance premiums tax deductible?

Usually no for personal policies.

Final Verdict

In most situations, life insurance payouts are one of the few major financial benefits that beneficiaries can receive completely tax-free.

However, taxes may still apply in certain situations involving:

- Interest earnings

- Estate taxes

- Cash value gains

- Policy transfers

Understanding these rules can help families and policyholders make smarter financial and estate planning decisions.

Conclusion

Life insurance provides valuable financial protection and peace of mind for families, but understanding the tax rules is equally important.

Before purchasing or structuring a policy:

- Review beneficiary designations

- Understand estate implications

- Learn how cash value taxation works

- Consult professionals for large estates

The right planning strategy can help maximize the financial benefits of life insurance while minimizing potential tax complications in 2026 and beyond.