Having an insurance claim denied can feel frustrating, stressful, and financially overwhelming. Whether it involves:

- Health insurance

- Auto insurance

- Home insurance

- Life insurance

A denial does not always mean the final answer is “no.”

Many denied claims are later approved after proper appeals and disputes.

Understanding how to challenge a denial can help you:

- Protect your finances

- Recover compensation

- Correct insurer mistakes

- Improve your chances of approval

In this complete 2026 guide, you’ll learn exactly how to dispute an insurance claim denial step by step.

What Is an Insurance Claim Denial?

An insurance claim denial occurs when an insurance company refuses to pay part or all of a submitted claim.

This means the insurer believes:

- The claim is not covered

- Policy conditions were violated

- Documentation is insufficient

- The claim was filed incorrectly

Common Types of Insurance Claim Denials

Claim denials can happen with many insurance products, including:

- Health Insurance

- Auto Insurance

- Homeowners Insurance

- Life Insurance

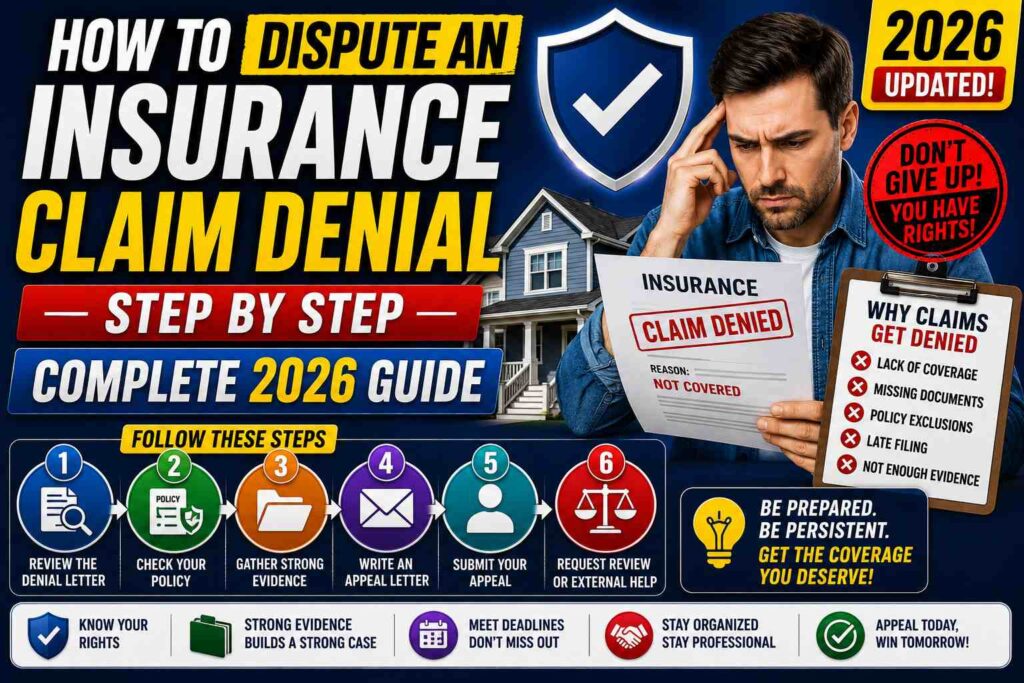

Common Reasons Insurance Claims Are Denied

Lack of Coverage

The policy may exclude the specific incident or damage.

Missed Deadlines

Claims filed too late may be rejected.

Incomplete Documentation

Missing:

- Photos

- Medical records

- Receipts

- Police reports

Can lead to denial.

Policy Lapses

Coverage may have expired due to missed premium payments.

Suspected Fraud

Insurers investigate suspicious or inconsistent claims carefully.

Pre-Existing Conditions

Some health insurance claims are denied because of policy limitations.

Insufficient Evidence

The insurer may argue the damages or losses are not adequately proven.

Also Read: Gig Worker Insurance Options 2026: Best Coverage for Freelancers

Can You Dispute an Insurance Claim Denial?

Yes.

Most insurance companies provide formal appeal processes that allow policyholders to challenge denied claims.

Many disputes succeed when:

- Strong evidence is provided

- Errors are corrected

- Additional documentation is submitted

Step 1: Carefully Review the Denial Letter

The denial letter explains:

- Why the claim was denied

- Relevant policy sections

- Appeal deadlines

- Next steps

Read it very carefully.

Why Reviewing the Denial Matters

Understanding the exact denial reason helps you:

- Build stronger evidence

- Correct mistakes

- Focus your appeal strategy

Simple Insurance Appeal Formula

\text{Strong Documentation} + \text{Policy Evidence} = \text{Higher Appeal Success Chance}

Step 2: Review Your Insurance Policy

Read the policy thoroughly, including:

- Coverage terms

- Exclusions

- Conditions

- Deductibles

- Filing requirements

Pay special attention to:

- The section referenced in the denial letter

- Definitions and exclusions

Step 3: Gather Supporting Evidence

Strong evidence is extremely important during disputes.

Useful Supporting Documents

For Health Insurance

- Medical records

- Doctor letters

- Treatment history

- Prescriptions

For Auto Insurance

- Accident reports

- Photos

- Witness statements

- Repair estimates

For Home Insurance

- Property damage photos

- Contractor estimates

- Receipts

- Inspection reports

For Life Insurance

- Death certificates

- Medical history

- Policy documents

Step 4: Contact the Insurance Company

Sometimes denials happen because of:

- Administrative errors

- Missing information

- Miscommunication

Calling the insurer may help resolve issues quickly.

During the call:

- Stay calm and professional

- Take notes

- Record names and dates

- Ask for clarification

Step 5: File a Formal Appeal

If the issue is not resolved informally, submit an official appeal.

What an Appeal Letter Should Include

- Policy number

- Claim number

- Explanation of dispute

- Supporting evidence

- Requested resolution

Appeal Letter Structure

A strong appeal letter should:

- Clearly explain why you disagree

- Reference policy wording

- Include supporting evidence

- Request reconsideration

Step 6: Meet Appeal Deadlines

Insurance appeals often have strict deadlines.

Missing deadlines can:

- Eliminate appeal rights

- Delay resolution

- Permanently close the claim

Typical Appeal Deadlines

| Insurance Type | Common Appeal Window |

|---|---|

| Health Insurance | 30–180 days |

| Auto Insurance | 30–60 days |

| Home Insurance | 30–90 days |

| Life Insurance | Varies by insurer |

Step 7: Request an Internal Review

Many insurers offer internal review processes where another claims specialist reevaluates the denial.

This can sometimes reverse incorrect decisions.

Step 8: Request an External Review

Some insurance types allow independent third-party reviews.

External reviewers are not employed by the insurance company.

This is especially common with:

- Health insurance disputes

- Large claim denials

Step 9: File a Complaint With Regulators

If you believe the insurer acted unfairly, you may contact:

- Insurance regulatory agencies

- Consumer protection offices

- State insurance departments

These organizations may investigate the insurer’s conduct.

Step 10: Consider Professional Help

Large or complicated disputes may require experts such as:

- Insurance attorneys

- Public adjusters

- Consumer advocates

This is especially useful for:

- High-value claims

- Bad faith denials

- Complex legal disputes

What Is Insurance Bad Faith?

Insurance Bad Faith occurs when insurers unfairly deny or delay legitimate claims.

Examples include:

- Unreasonable delays

- Ignoring evidence

- Misrepresenting policy terms

- Refusing proper investigation

Signs Your Denial May Be Wrong

Contradictory Explanations

The insurer changes denial reasons repeatedly.

Missing Investigation

The company refuses to inspect evidence properly.

Policy Language Supports Coverage

Your policy wording appears to cover the claim.

Similar Claims Were Previously Approved

This may suggest inconsistent claim handling.

Tips to Improve Your Chances of Winning an Appeal

Stay Organized

Keep:

- Emails

- Photos

- Medical records

- Letters

- Receipts

Communicate Professionally

Remain calm and factual.

Use Policy Language

Referencing policy wording strengthens arguments.

Act Quickly

Fast responses help prevent delays.

Document Everything

Keep detailed records of:

- Phone calls

- Emails

- Dates

- Conversations

Common Mistakes During Insurance Disputes

Ignoring Deadlines

Late appeals may be rejected automatically.

Submitting Weak Documentation

Strong evidence is critical.

Becoming Emotional

Aggressive communication rarely helps.

Accepting the First Denial Without Question

Many valid claims are later approved after appeals.

Can Insurance Companies Reverse Denials?

Yes.

Claims are sometimes approved after:

- Additional evidence

- Internal review

- Legal pressure

- External appeals

How Long Does an Insurance Appeal Take?

Appeal timelines vary.

Estimated Appeal Timeframes

| Appeal Type | Estimated Time |

|---|---|

| Internal Review | Few weeks–2 months |

| External Review | 1–6 months |

| Legal Dispute | Several months or longer |

Why Insurance Claim Disputes Are Increasing in 2026

Disputes are becoming more common due to:

- Rising healthcare costs

- Expensive repairs

- More severe weather events

- Increased claim volumes

- Complex policy language

Consumers today must understand their appeal rights more than ever.

Frequently Asked Questions (FAQs)

Can I appeal a denied insurance claim?

Yes. Most insurers provide formal appeal procedures.

How do I dispute a claim denial?

Review the denial, gather evidence, and submit a formal appeal.

What documents help with insurance appeals?

Photos, receipts, medical records, repair estimates, and policy documents are often important.

How long do insurance appeals take?

Anywhere from a few weeks to several months depending on complexity.

Can lawyers help with denied insurance claims?

Yes, especially for large or complicated disputes.

Final Verdict

A denied insurance claim does not always mean the end of the process. Many claims are successfully overturned after proper disputes and appeals.

The key to improving your chances includes:

- Understanding your policy

- Gathering strong evidence

- Meeting deadlines

- Staying organized

- Communicating professionally

Knowing your rights can help protect your finances and ensure fair treatment from insurers.

Conclusion

Understanding how to dispute an insurance claim denial can make a major difference during stressful financial situations.

If your claim is denied:

- Don’t panic

- Review the denial carefully

- Build strong documentation

- Follow the appeal process properly

With persistence, preparation, and evidence, many policyholders successfully reverse denied claims and receive the compensation they deserve in 2026 and beyond.