Understanding health insurance terminology can feel confusing, especially when terms like deductible, copay, coinsurance, and out-of-pocket maximum are involved.

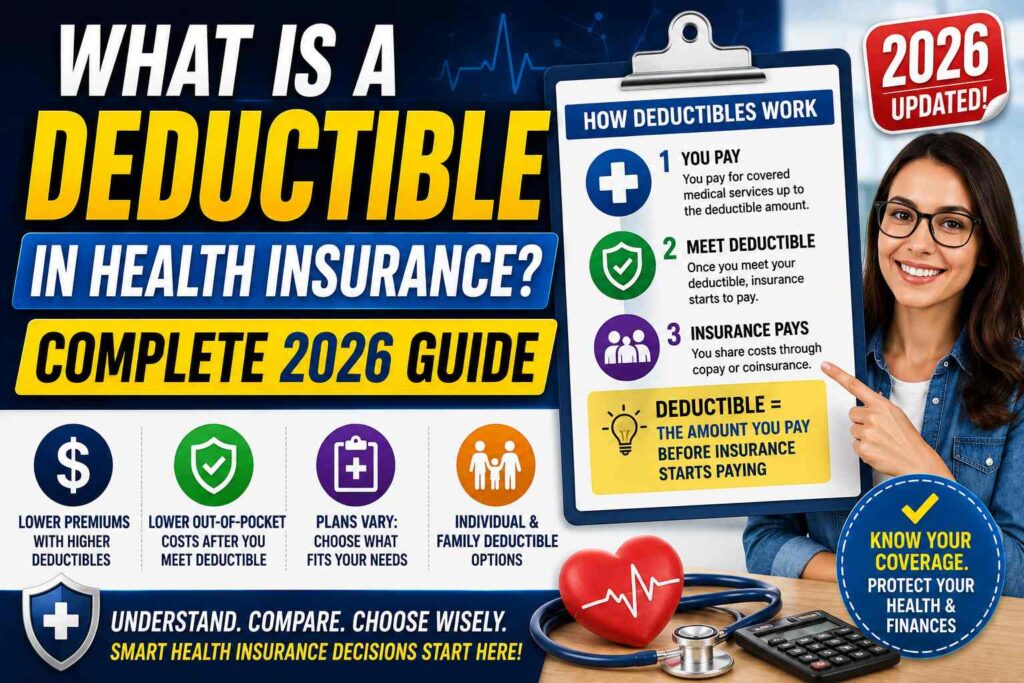

One of the most important concepts in Health Insurance is the deductible.

A deductible is the amount of money you must pay for covered medical services before your health insurance company starts sharing the costs.

In this complete guide, you’ll learn:

- What a deductible means

- How deductibles work

- Different types of deductibles

- Deductible vs copay

- High vs low deductible plans

- How to choose the right deductible in 2026

How Does a Health Insurance Deductible Work?

A deductible is the amount you pay out of your own pocket before your insurer begins paying for covered healthcare services.

Example of a Deductible

Imagine your health insurance plan has:

- $1,000 deductible

- 20% coinsurance after deductible

If you receive a medical bill of $5,000:

- You first pay the $1,000 deductible

- Insurance begins sharing costs afterward

- You may then pay 20% coinsurance on the remaining amount

Why Health Insurance Deductibles Exist

Insurance companies use deductibles to:

- Reduce unnecessary claims

- Share healthcare costs with policyholders

- Lower monthly premiums

- Encourage responsible healthcare spending

Plans with higher deductibles often have lower monthly premiums.

Also Read: Term Life Insurance vs Whole Life Insurance: Which One Is Better in 2026?

Types of Health Insurance Deductibles

Individual Deductible

Applies to one person covered under the policy.

Family Deductible

Applies to all members under a family health plan.

Once the family deductible is met, insurance coverage begins for all covered members.

Embedded Deductible

Each family member has an individual deductible within the family plan.

Aggregate Deductible

The total family deductible must be met before insurance begins paying.

Deductible vs Copay

Many people confuse deductibles and copays.

| Feature | Deductible | Copay |

|---|---|---|

| What It Is | Amount paid before insurance shares costs | Fixed fee for services |

| Payment Timing | Before coverage begins | During doctor visits or prescriptions |

| Example | $1,000 yearly deductible | $25 doctor visit copay |

Deductible vs Coinsurance

Deductible

The amount you pay before insurance contributes.

Coinsurance

The percentage you pay after meeting the deductible.

Example of Deductible and Coinsurance Together

Suppose you have:

- $2,000 deductible

- 20% coinsurance

Medical bill = $10,000

Step 1:

You pay the first $2,000 deductible.

Step 2:

Remaining amount = $8,000

Step 3:

Insurance pays 80%

You pay 20%

Your coinsurance payment:

0.20 \times 8000 = 1600

Total You Pay:

- Deductible: $2,000

- Coinsurance: $1,600

- Total: $3,600

High Deductible Health Plans (HDHPs)

High Deductible Health Plan usually have:

- Lower monthly premiums

- Higher deductibles

These plans are popular among:

- Young adults

- Healthy individuals

- Freelancers

- Gig workers

Benefits of High Deductible Plans

Lower Monthly Premiums

You pay less every month.

Health Savings Account (HSA) Eligibility

Many HDHPs allow you to open:

Health Savings Account

HSAs provide:

- Tax advantages

- Medical savings flexibility

- Long-term healthcare savings

Better for Healthy Individuals

If you rarely visit doctors, a higher deductible may save money overall.

Drawbacks of High Deductible Plans

Higher Out-of-Pocket Costs

Medical emergencies can become expensive.

Financial Stress

Large deductibles may be difficult for some families to afford.

Delayed Medical Care

Some people avoid treatment because of high upfront costs.

Low Deductible Health Plans

Low deductible plans generally offer:

- Higher monthly premiums

- Lower upfront medical costs

These plans are often better for:

- Families

- Seniors

- People with chronic conditions

- Frequent doctor visits

What Services Are Usually Exempt from Deductibles?

Many health plans cover preventive care before you meet your deductible.

Examples may include:

- Annual checkups

- Vaccinations

- Preventive screenings

- Wellness visits

Coverage varies by policy.

Also Read: Best Life Insurance for Young Adults in 2026: The Complete Guide

What Is an Out-of-Pocket Maximum?

The out-of-pocket maximum is the highest amount you must pay during a policy year for covered services.

After reaching this limit:

- Insurance typically pays 100% of covered costs

Difference Between Deductible and Out-of-Pocket Maximum

| Feature | Deductible | Out-of-Pocket Maximum |

|---|---|---|

| Definition | Amount before insurance shares costs | Maximum yearly spending limit |

| Includes | Initial healthcare costs | Deductibles, copays & coinsurance |

| Purpose | Cost sharing | Financial protection |

Average Health Insurance Deductibles in 2026

Deductibles vary widely depending on plan type and location.

Estimated Average Deductibles

| Plan Type | Average Deductible |

|---|---|

| Employer-sponsored plan | $1,500–$2,500 |

| Marketplace individual plan | $3,000–$7,500 |

| HDHP | $5,000+ |

How to Choose the Right Deductible

Choose a Higher Deductible If You:

- Are healthy

- Rarely visit doctors

- Want lower premiums

- Have emergency savings

Choose a Lower Deductible If You:

- Need regular medical care

- Have chronic conditions

- Prefer predictable costs

- Have a family

Common Health Insurance Deductible Mistakes

Focusing Only on Premiums

Lower premiums may mean much higher deductibles.

Ignoring Total Healthcare Costs

Consider:

- Copays

- Coinsurance

- Prescription costs

- Out-of-pocket maximums

Not Understanding Coverage Rules

Always review:

- Network providers

- Exclusions

- Deductible structure

Deductibles in Family Health Plans

Family plans often include:

- Individual deductibles

- Overall family deductible limits

This can become complicated, so understanding your policy details is important.

Are Prescription Drugs Subject to Deductibles?

Sometimes yes.

Some plans:

- Apply deductibles to prescriptions

- Offer copays immediately

- Separate medical and pharmacy deductibles

Can Preventive Care Be Free Before Deductible?

Yes. Many plans cover preventive services without requiring you to meet the deductible first.

This may include:

- Vaccines

- Screenings

- Wellness exams

Why Deductibles Matter in 2026

Healthcare costs continue rising globally, making deductibles more important than ever.

Consumers are increasingly choosing plans based on:

- Monthly affordability

- Healthcare usage

- Financial flexibility

- Emergency preparedness

Understanding deductibles helps you avoid unexpected medical expenses.

Frequently Asked Questions (FAQs)

What is a deductible in health insurance?

A deductible is the amount you pay for healthcare services before your insurance starts sharing costs.

Is a high deductible good or bad?

It depends on your health needs and financial situation.

Do I pay deductible for every doctor visit?

Not always. Some services may only require a copay.

What happens after I meet my deductible?

Insurance begins sharing covered healthcare costs according to your policy terms.

Are deductibles yearly?

Most health insurance deductibles reset annually.

Final Verdict

A health insurance deductible is one of the most important parts of any health plan. It directly affects:

- Monthly premiums

- Out-of-pocket costs

- Financial risk

- Healthcare affordability

Choosing the right deductible depends on your:

- Health condition

- Budget

- Medical usage

- Risk tolerance

Understanding how deductibles work can help you make smarter healthcare and financial decisions in 2026.

Conclusion

Health insurance deductibles can seem confusing at first, but they play a major role in determining how much you pay for medical care.

Before choosing a plan:

- Compare deductibles carefully

- Review total costs

- Estimate your medical needs

- Understand coinsurance and copays

The best health insurance plan is one that balances affordability with financial protection for your specific situation.